Semiconductors are vital for a seat at the G7 table

The design, fabrication and sale of semiconductor devices across a wide range of materials, with an ever-expanding range of properties, supports a rapidly expanding range of applications. As such, semiconductors, and the semiconductor design and fabrication tools to create them have become fundamental enablers of our modern way of life and our economy.

It is well reported that one job in the industry supports another five to seven jobs in the wider economy (SIA), and although successful chip companies require a lot of investment over a long term, the rewards, in revenue and valuation, can be huge. Many of the key inventions which enable entire downstream industries are based in the materials science, circuit design, or system architecture developed by the engineers in these companies. This is why Nvidia is so valuable, as they are now the foundational technology behind the global AI boom.

If we cannot build and retain UK companies which deliver globally relevant technology into the broad microelectronics/photonics industry, which enables all of quantum, AI, energy, robotics, etc etc. then in 15 years’ time, the UK will become an interesting, underdeveloped country with people from wealthy nations visiting to reminisce about bygone times, buying tourist curiosities from our previously skilled society, as we slip into irrelevance.

In the coming decades, any developed nation which does not have a role to play in this global industry will decline in geopolitical relevance. As oil and gas were once the economic drivers of global hegemony, so now it is prowess in semiconductor technology which defines the world order, through enablement and control of emerging technologies, such as AI, Quantum, Communications, Cryptosecurity, Robotics, Renewable energy, etc. These transformative technologies are now driving the focus of the G7 group of leading economies and, as such, our seat at the G7 table will depend on the UK’s credibility in this crucial sector.

Putting aside the influence of Taiwan and the billions of dollars being pumped into Arizona to build chips, how can we even compete with Dresden or Crolles in semiconductors?

The UK has a historic strength in microelectronic device and systems design (e.g. Alphamosaic, ARC, ARM, CamSemi, CSR, Dialog, Graphcore, ICL, Icera, Imagination, Raspberry Pi, Wolfson). We also have a strong research and innovation base in materials science, photonics and innovative compound and thin film device fabrication (e.g. Pragmatic, Paragraf, Kubos, Plessey), with previous academic research translated into start-ups and innovative SMEs.

The biggest problem we face is scaling those SMEs into companies able to supply globally to end-users and with a clear understanding of ‘product-market’ fit. Whereas the US, EU and Chinese administrations have prioritised public / private investment into tech industries for decades, the UK has been slow to realise the importance of this critical sector.

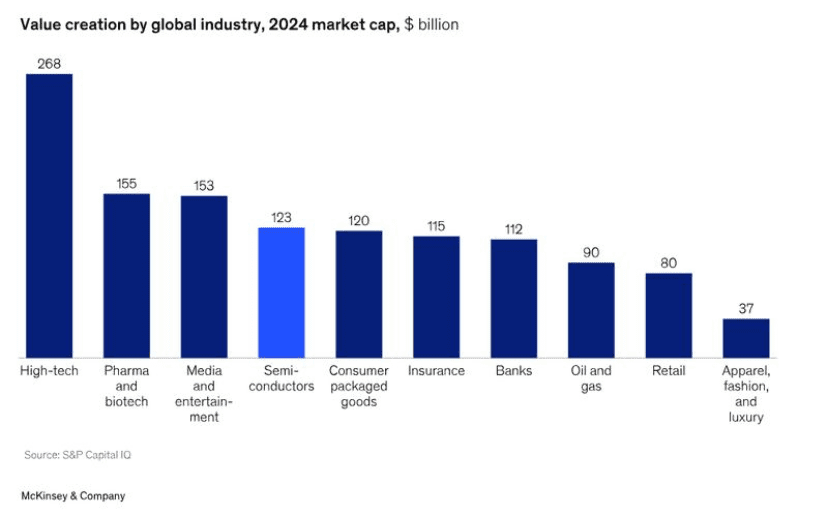

Semiconductors are the fourth largest global industry, and key for the first Source: McKinsey & Co

The opportunity now, is to focus on what comes after the sub-10nm silicon digital CMOS fabs costing 10’s billions a piece and instead ‘shoot ahead of the puck’ to the future, where low power neuromorphic processors will replace 2nm CMOS GPUS, high performance, low power photonic computing will displace traditional data centers, advanced wide-bandgap materials will enable breakthroughs in energy generation, distribution and storage and thin film and 2d materials will enable new sensors and applications in food, health and agri-tech.

Where the UK can design here and manufacture overseas (using those legacy $10’s billions fabs) we should, elsewhere, the proprietary materials know-how will mean we should and must invest to grow that capacity at home.

You’ve warned that if the UK doesn’t address the semiconductor skills gap, it will cease to be a significant global power. Is the UK truly doing enough to attract young people into engineering and deep tech, or are we still facing the same ‘brain drain’ that we have for the last forty years.

This is such a ‘boil the ocean’ question. We could always do more, but I really do think that we all (government, industry and academia) are working hard now to address the skills gap. Short term, the only solution is to address visa and immigration issues to ensure firms can hire the best and right sort of talent (which needs to stay here). Secondly, we should ensure that when graduates leave university or apprentices leave college, they are motivated / guided into valuable careers in microelectronics and not lost to other career options – this is part of the STEP program right now. In the medium term, we must get more secondary school children into STEM degrees and apprenticeships. But here, any intervention now will take ~7 years before we see a workforce improvement, and this requires broader public education of the opportunities (since we need to affect GCSE and A Level choices).

Finally, in the longer term, the fundamental problem we face is that, public knowledge of and respect for this critical sector is very low. The notion of being interested in and / or studying STEM or electronics, etc. is to be looked down upon and seen as geeky, or boring. The truth of course is markedly different, and I think government and industry have a lot of work to do here, to drive an excitement and keenness across society to be part of a tech revolution which will radically overshadow the industrial revolution. We need to reach a point where families celebrate a student’s successful GCSE test-chip, in the same way as whole families in Taiwan celebrate when a student joins TSMC as a new starter.

What will the National Semiconductor Centre mean for the industry. Is this not just a repeat of the National Microelectronics Institute? How do we avoid this becoming yet another white elephant or guarding a gateway?

Well, the National Microelectronics Institute, is of course, the trade association for semiconductor manufacturing and supply chain since 1996 and has been very successful since then as a convening point for the UK semiconductor industry. The National Semiconductor Centre (NSC) on the other hand is to be set up by government as an arm’s length body, funded to serve as a central coordination body between government, industry and academia, providing a single point of contact on technology roadmaps, policy, strategy and funding and to represent the UK internationally.

TechWorks and other relevant independent industry groups are expected to and must be closely involved with the NSC. I think the success of the NSC is partially up to us, to ensure we stay close and keep it well aligned to industry needs.

How can the UK semiconductor industry capitalise on its advantages? What do we need to do?

Three things. Investment (public and private can support each other here), Ambition (set a personal goal to be a global player while still owned here, don’t cash out early), Build supply chains and ecosystems in the UK where possible to foster local partnerships (government must support this through funded missions – scale-up not just innovation funding, public procurement can help). We don’t have to do what everyone else is doing, there is plenty else for us to focus on.

Can we afford to do that?

Yes, the cost of a pilot-volume scale up fab at a ‘legacy’ node (which is relevant for eg photonics, quantum, power electronics, RF, sensors) is significantly less than $1bn. The cost of building a fabless chip company to a commercially sustainable level can be achieved with half a $bn investment. The UK Dept for Science and Tech’s R&D budget next year will be £15.2bn, with UKRI receiving £8.8bn of that. A public investment of £1bn matched by private money and spent wisely would be transformative in scaling the numerous SMEs and ‘stuck-at-series-A’ companies in the UK, who’s current only option is to look for overseas acquirers.

What parts of the UK supply chain are missing that we need? Does design need a manufacturing base?

Advanced CMOS design for next-gen compute, communications and so forth are well served by global advanced CMOS fabs. However, to get access to those fabs without putting a down-payment on one of their lines (a $bn business!), we need to negotiate international access and here, we can leverage other intellectual property and national capabilities aka ‘seat at the table’.

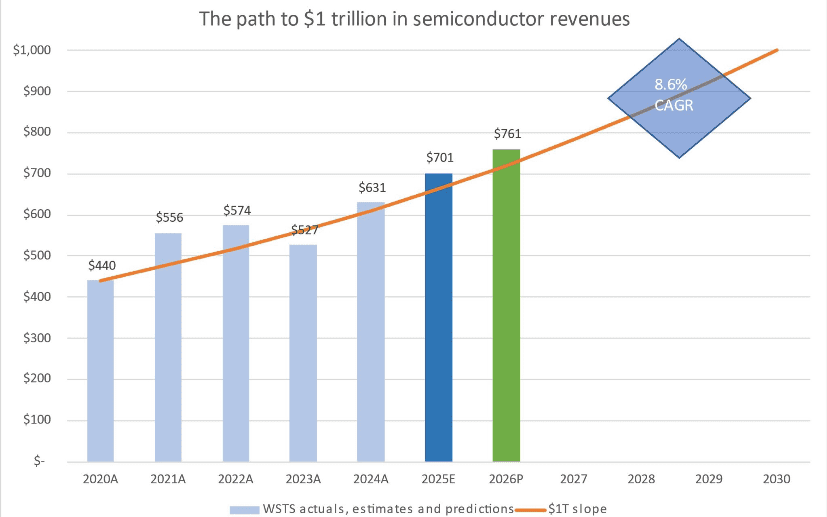

The path to $1rilliion Source: WSTS June 2025

However, a lot of our unique capabilities are in novel and advanced materials and non-digital silicon design. Here, much of the unique design value is inextricably intertwined with the fabrication process itself. The design is only possible because of the novel process. The process is created specifically in order to make the design possible. Especially where this novelty enables a new class of device, or perhaps even a new market, then the UK really must double down and create the local supply chain. It is this very scenario, where we have a unique first-mover opportunity to nurture a world-class supply chain as it grows, ultimately into a significant new market. Or we allow others to license the IP, (majority) invest in and acquire those businesses and ultimately cede that market to others. Good examples of these would be photonics, mems, wide-bandgaps, thin films, 2d materials and advanced packaging.

Can we go back to a global supply chain, or is sovereign capability necessary and inevitable?

I don’t think we ever left ! – what’s changed is that people now worry about provenance and security of supply. Also, some national administrations (which understand the global importance of semiconductor technology), recognise the need to obtain as much control as they realistically can over supply chains, in the same way that oil was the global economic / political currency of the last century.

Going forward, we must collaborate and trade with our global neighbours, whilst keeping one eye on our own back yard to make sure we are growing enough to feed our own family!

If you got a meeting with the Prime Minister, what would you ask for?

Two or three national missions with a fully joined up collaboration plan and supply chains from innovation through product scale up into specific future end-market sectors and fully funded with public-private partnership and gov procurement. All actors identified and where they are missing, a plan of how we plug the gap with UK capability or worst-case a close-ally and friendly neighbor. The objective of each of these would be not just to ensure resilience and security, but creation and retention of jobs over a range of skill levels and a significant tax-take (GVA) for the UK economy from commercially successful companies at the right-hand end of the TRL line. Ultimately owned by UK entities.

Charles Sturman joined TechWorks in 2023 following leadership roles at Neul, u-blox, Arm, Motorola, TTP Com and the deep tech start-up Cognovo. With expertise gained in start-ups, SMEs and global enterprises, Sturman is also Chair of the Alliance of IOT Innovation, and an advisor to Silicon Catalyst, Cambridge Deeptech Labs and Cambridge Wireless. TechWorks has established a novel membership model based around a series of Connected Communities. Each Community serves a group of member’s interest whilst at the same time remains connected to a wider ecosystem enabling cross-domain connections and working on common challenges, and the group has contributed to the UK industrial strategy.

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :

If you enjoyed this article, you will like the following ones: don't miss them by subscribing to :